Real Product Is Not Idealism. It’s Independence.

Why the most cold-blooded, pragmatic move in a broken acquisition market is building something people actually need

If you look at the mobile app market today, you won’t see a sudden, dramatic crash. There are no spectacular explosions. Instead, we are witnessing a slow, creeping catastrophe—a quiet tightening of the screws that has been compounding for several years.

It started back when Apple introduced App Tracking Transparency, throwing a wrench into the machinery of mobile advertising. But over the last eighteen months, the pressure has reached a tipping point, especially in the consumer health, wellness, and longevity sectors. In these niches, companies aren’t just selling software; they are selling hope. And whenever a market trades in hope, the underlying economics can get incredibly messy.

For a long time, the industry relied on a playbook that was highly transactional. You bought cheap traffic, made a grand promise to fix the user’s life by Monday, and pushed them through an interminable, pseudo-scientific onboarding quiz. You called the output a “personalized plan,” collected the subscription fee, and hoped they would forget to cancel. It didn’t matter if they actually used the app—the math worked, the subscription retention looked good enough on paper, and investors kept writing checks.

That machine is now cracking. Not because people have stopped caring about their health, but because the very nature of mobile distribution has fundamentally changed.

The App Store is now a paid shelf

The App Store is no longer a neutral directory where a great product organically finds its audience. It has become a heavily monetized, paid shelf.

Apple’s own data tells us that 70% of App Store visitors use search to find apps, and nearly 65% of downloads happen immediately after a search query.[^1] This means the single most valuable asset in the ecosystem is the user’s active intent. When someone types “sleep tracker” or “anxiety,” they are ready to act.

Apple’s own App Store discovery data:

70% of App Store visitors use search to discover apps

~65% of downloads happen directly after a search query

60%+ conversion rate for ads at the top of search results

Source: Apple Ads — “Ads on the App Store”.

Naturally, Apple has monetized this intent. Apple Search Ads aren’t just an optional marketing channel; they are a toll booth at the entrance to your organic demand. Even if you have spent years building a stellar product, earning thousands of genuine five-star reviews, and establishing brand trust, you still have to pay Apple to defend your own brand name from competitors bidding on it.

With Apple’s recent expansion of ad slots further down the search results,[^2] the space left for pure organic discovery has shrunk even more. This isn’t just a minor inflation of cost-per-tap; it is a structural shift. The platform is systematically clawing back the organic real estate that developers used to earn through quality, forcing independent teams to buy back their own audience. Every dollar spent defending your search listing is a dollar taken directly out of product development, customer support, and actual innovation.

The pollution of the digital marketplace

To make matters worse, the App Store has become an incredibly noisy, manipulated environment. Honest developers aren’t just competing against better products; they are competing against click farms, black-hat SEO, review manipulation, and copycat apps designed to extract quick cash and disappear.

Again, this isn’t cynical speculation. Here is what Apple itself removed in 2024 alone:

What Apple removed in 2024 alone:

143M+ fraudulent ratings & reviews

7,400+ apps pulled from the charts

9,500+ deceptive apps banned from search results

Source: Apple, “The App Store prevented more than $9 billion in fraudulent transactions”, 2025.

When cleanup operations have to happen at this scale, the term “organic growth” starts to lose its meaning. You are forced to compete in an auction against bad actors who have no intention of building a long-term business, but who are perfectly happy to drive up acquisition costs for everyone else while they monetize user confusion.

The regulatory and optimization tax

For health and wellness apps, the battlefield is even more treacherous. In the wake of high-profile FTC actions against platforms like BetterHelp and GoodRx over the unauthorized sharing of sensitive health data via tracking pixels, the major advertising networks panicked. BetterHelp’s $7.8 million settlement and strict ban on sharing health data for ad targeting sent shockwaves through the industry.[^4]

Consequently, advertising platforms have dramatically tightened their policies. Meta’s restrictions on health and wellness advertisers have made it incredibly difficult to optimize campaigns using lower-funnel events like “Purchase” or “Add to Cart.” Instead, developers are forced to optimize for weaker top-of-funnel signals like landing page views.[^5]

This is where the unit economics truly break down. When an ad algorithm can no longer see who actually buys your product, it stops learning. It starts buying noise. You end up paying for clicks from people who look interested but never convert. To compensate, marketing teams have to run endless creative testing, build dozens of compliant landing pages, and constantly guess what will get flagged by policy bots next.

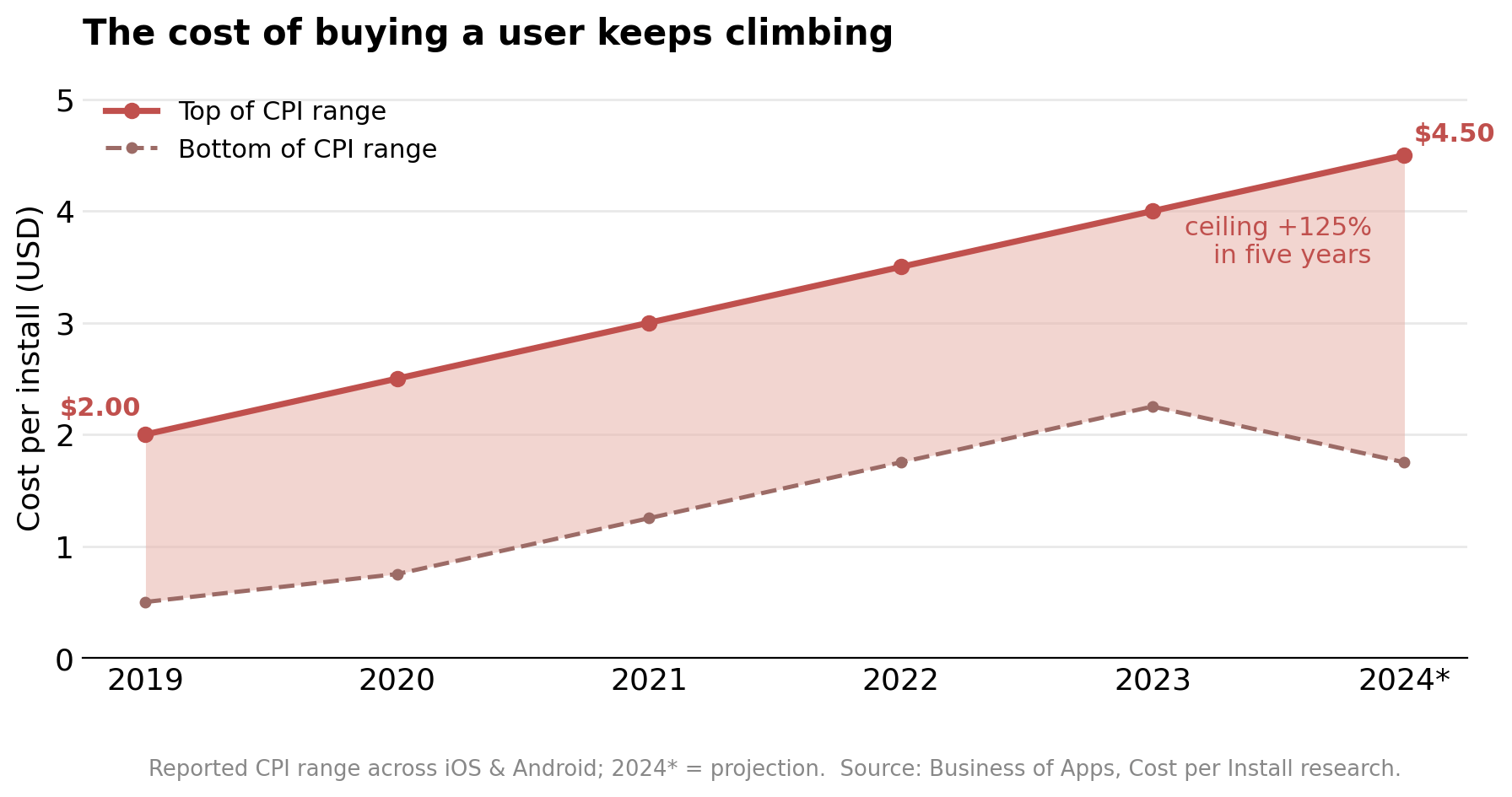

Health apps are no longer just paying for media; they are paying a steep privacy risk premium, a compliance tax, and an optimization penalty. And the base price of a user was already climbing long before any of this — the reported cost-per-install range has drifted up year after year, with the high end more than doubling since 2019.[^9]

The AI supply shock and the wearable moat

Then came the rise of generative AI.

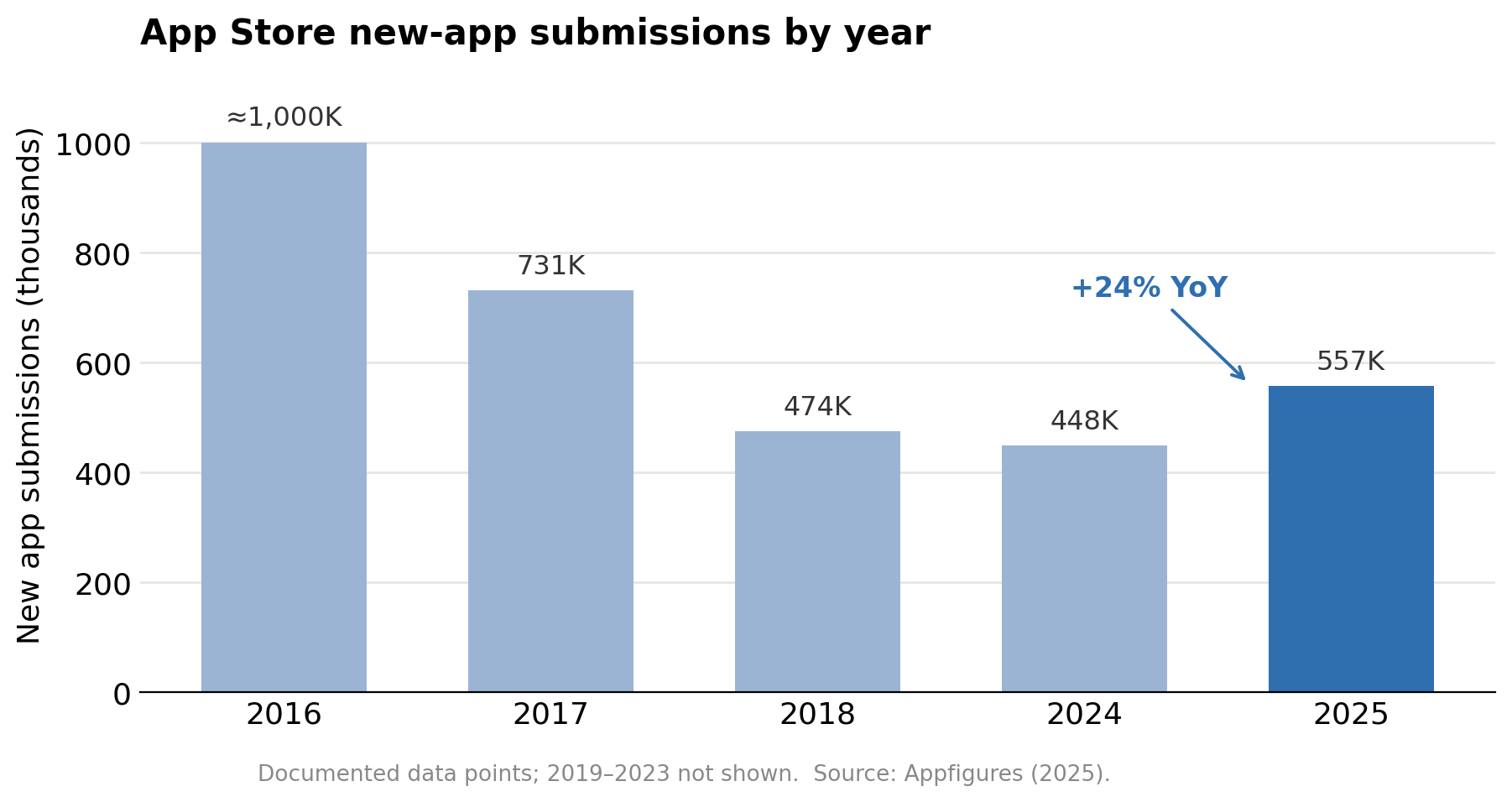

In 2025, the App Store saw 557,000 new app submissions—a massive 24% jump year-over-year, and the first meaningful increase since the 2016 peak.[^6] While it has never been easier or cheaper to write code and ship an app, it has never been harder or more expensive to get noticed.

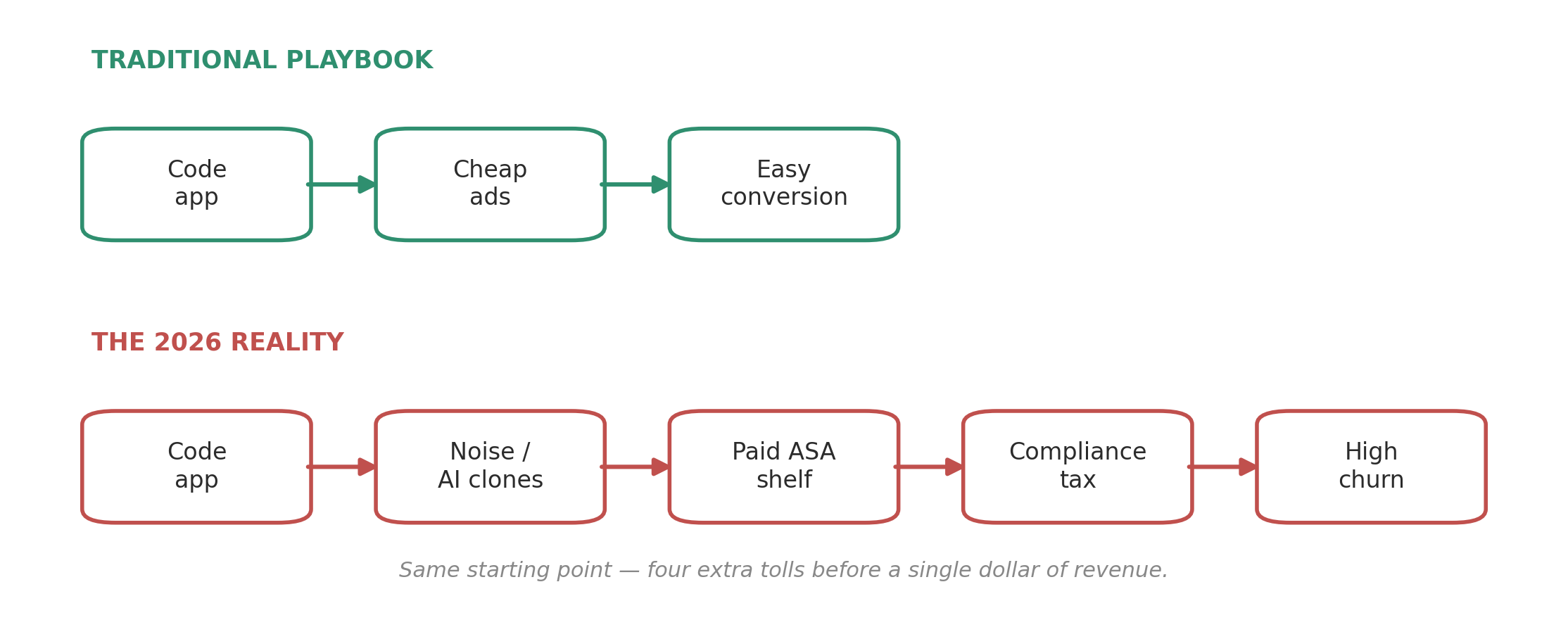

The market is flooded with weekend projects, wrapper apps, and generic AI “coaches” that look slick in screenshots but offer zero depth. They still bid on your keywords, clutter search results, and dilute user trust in the entire category. Code has been commoditized, making distribution the only real moat.

The starting point is identical for everyone. What changed is everything that now sits between shipping an app and earning a dollar:

Furthermore, independent software developers are finding themselves outmatched by hardware and ecosystem giants. Wearable players like Oura, Garmin, Whoop, and Apple do not need to make the unit economics of a standalone app work. They treat software as a retention mechanism for their high-margin physical devices or broader ecosystems. They can afford to lose money on software services indefinitely because the hardware or ecosystem lock-in pays for it. Independent founders, on the other hand, have to run an actual, self-sustaining business.

This summer will be a graveyard for weak economics

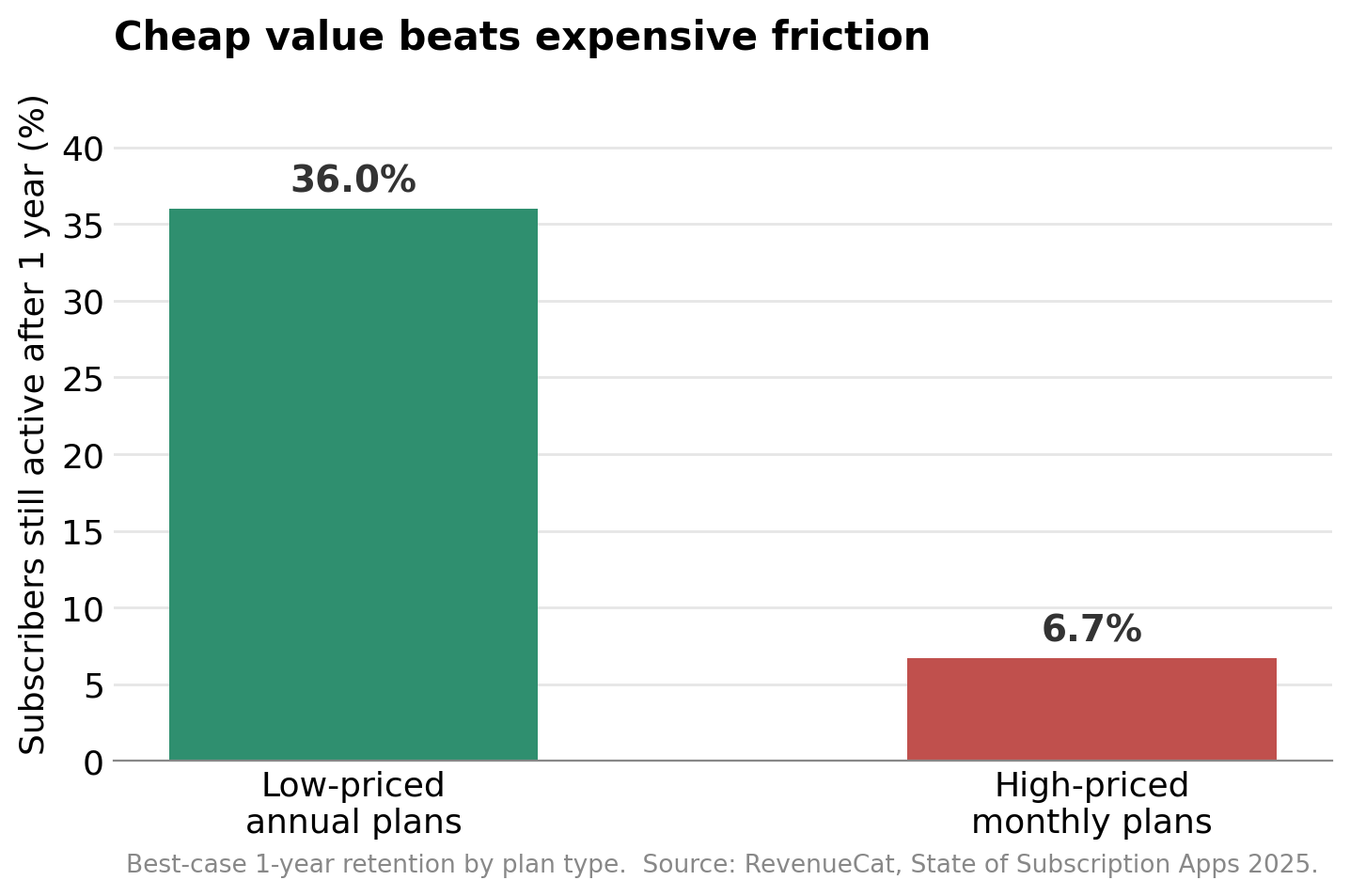

The old playbook of buying cheap traffic, selling a generic promise, and relying on high-friction subscription retention is fundamentally dead. The data from RevenueCat’s subscription report proves it: nearly 30% of annual subscriptions are canceled within the first month.[^7] And cheap, sticky value beats an aggressive paywall every time — low-priced annual plans keep up to 36% of subscribers after a year, while high-priced monthly plans hold just 6.7%.[^7]

If your product is nothing more than an aggressive paywall with a basic questionnaire behind it, your payback period is going to stretch out to infinity.

We are already seeing the casualties of this shift. High-profile, well-funded players across the digital health and wellness spectrum are quietly shutting down or restructuring:

Health & wellness players that wound down or restructured:

Care/of — personalized vitamins (Bayer-owned). Shut down, subscriptions canceled — 2024.

Forward — tech-enabled primary care, ~$657M raised at a $1B valuation. Closed all locations, app shut down — 2024.

Modern Age — VC-backed longevity clinics. Closed after failing to secure capital — 2024.

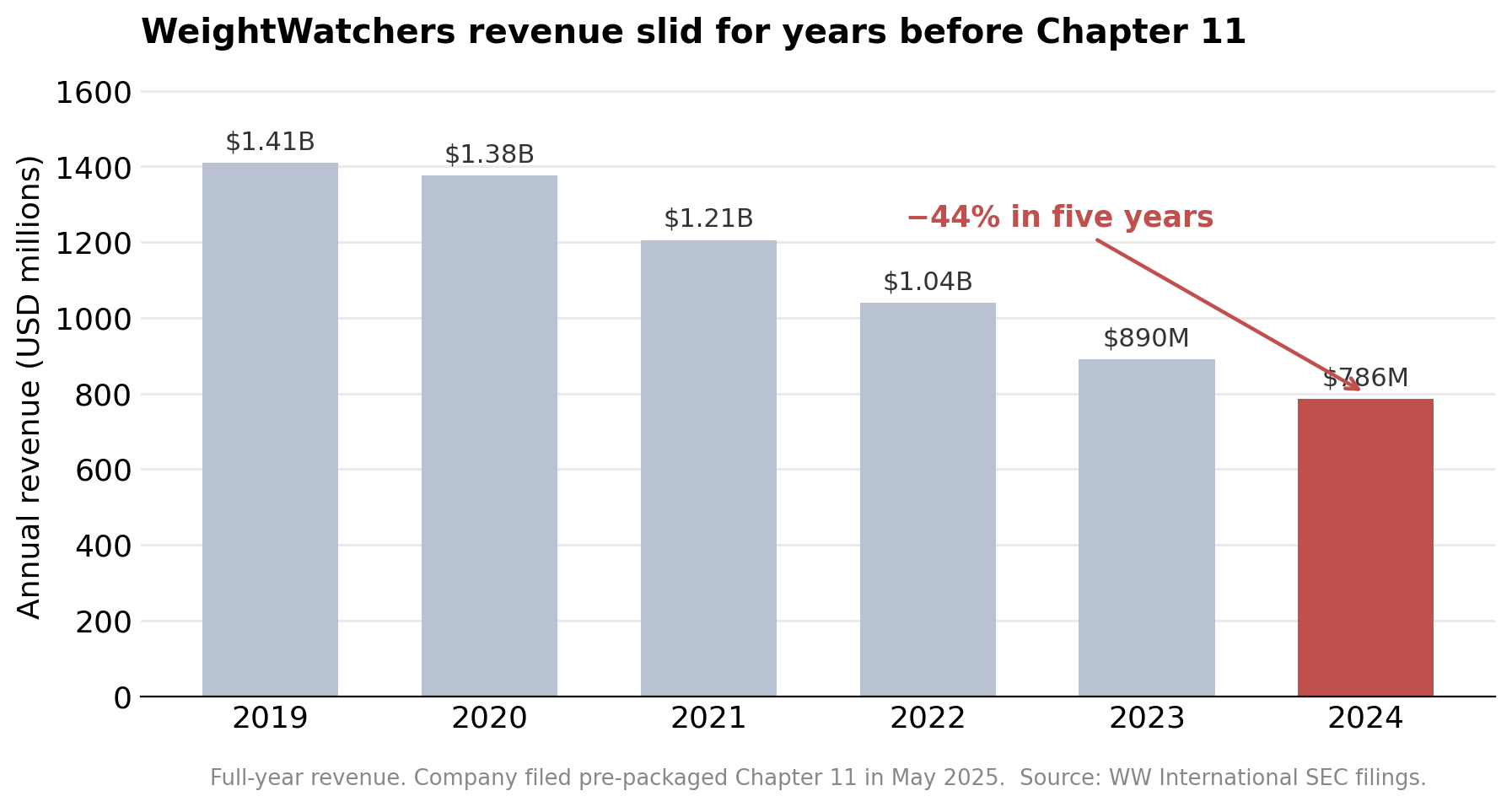

WeightWatchers — public weight-management company (NASDAQ: WW). Chapter 11 to restructure debt, pivoting to GLP-1 — 2025.

Sources: TechCrunch, Fierce Healthcare, Longevity.Technology, SEC filings.

WeightWatchers is the most visible example — a public company whose top line slid for years before the filing. Revenue fell from $1.41 billion in 2019 to $785.9 million in 2024, a 44% drop, and in May 2025 it entered a pre-packaged Chapter 11 to restructure its debt.[^10]

These companies didn’t fail simply because “CPI went up.” They failed because demand does not equal a viable business model. When venture capital dries up and cheap acquisition disappears, a pretty mission statement cannot save you from the cold reality of retention and cash flow.

Many teams that spent the last few years scaling via aggressive performance marketing instead of building deep product value are going to hit a wall.

Why product-first is a survival strategy, not romance

For years, investing heavily in product quality, deep technical integrations, and real user utility looked almost naive.

In every boardroom, there is always someone asking: Why are we spending so much on R&D? Why not just pump that money into UA? Why not make the paywall more aggressive? Why not copy the competitors’ onboarding flow? When capital was cheap and ad platforms were highly efficient, those voices often sounded right. You could brute-force growth through marketing and fix the product “later.”

But when the tide goes out, you finally see who was swimming naked.

Building a product that actually delivers value, retains users through genuine utility, and drives organic word-of-mouth isn’t a romantic, idealistic choice. It is the most cold-blooded, pragmatic business strategy available to an independent founder.

After ten years of building Welltory, I can look at our shareholders and say with absolute certainty: the long-term investment we made in our product—even when it seemed slow and inefficient—is the exact reason we are still standing while others are winding down.

When you build something people actually need, you earn “user money.” And user money is the cleanest capital in the world. It doesn’t come with board seats, liquid preferences, or demands for irrational growth. It gives you oxygen, independence, and the leverage to say “no” to bad decisions.

If you are a founder who has been criticized for being too product-driven, too stubborn about quality, or too slow to squeeze your users for short-term revenue, let this market shift validate your instincts. You are not being naive. You are building the only type of business that can survive an expensive, noisy, and highly manipulated distribution landscape.

When the noise gets louder, when the ad platforms change their algorithms again, and when the market is flooded with a million more AI clones, the only ground you will have under your feet is the fact that real users find real value in what you built.

That isn’t a fairy tale. That is survival.

Sources

[^1]: Apple Ads — Ads on the App Store. 70% of App Store visitors use search to discover apps; almost 65% of downloads happen directly after a search; conversion at the top of search results runs over 60%. https://ads.apple.com/app-store

[^2]: eMarketer — Apple expands App Store search ads; advertisers will soon reach high-intent users (2026). Apple is adding ad placements beyond the single top slot, further down the search results, rolling out from March 3, 2026 (UK and Japan first, then globally). https://www.emarketer.com/content/apple-expands-app-store-search-ads-reach-high-intent-users

[^3]: Apple Newsroom — The App Store prevented more than $9 billion in fraudulent transactions (May 2025). In 2024 Apple removed 143M+ fraudulent ratings and reviews, 7,400+ apps from the charts, and nearly 9,500 deceptive apps from search results. https://www.apple.com/newsroom/2025/05/the-app-store-prevented-more-than-9-billion-usd-in-fraudulent-transactions/

[^4]: U.S. Federal Trade Commission — FTC Gives Final Approval to Order Banning BetterHelp from Sharing Sensitive Health Data for Advertising, Requiring It to Pay $7.8 Million (2023); followed the FTC’s $1.5M action against GoodRx. https://www.ftc.gov/news-events/news/press-releases/2023/07/ftc-gives-final-approval-order-banning-betterhelp-sharing-sensitive-health-data-advertising

[^5]: Foley Hoag LLP — Meta’s New Advertising Rules: Key Considerations for Health and Wellness Businesses (Jan 2025). Practitioner detail on the loss of lower-funnel events (Purchase / Add to Cart) and the forced shift to weaker signals: Polar Analytics, 2025 Meta’s Tracking Restrictions for Health & Wellness. https://foleyhoag.com/news-and-insights/blogs/security-privacy-and-the-law/2025/january/meta-s-new-advertising-rules-key-considerations-for-health-and-wellness-businesses/ · https://www.polaranalytics.com/post/2025-metas-tracking-restrictions-for-health-wellness-are-here----heres-how-to-fix-it

[^6]: Appfigures — The App Store Just Logged Its Biggest Release Year in Nearly a Decade (Dec 2025). 557K new App Store submissions in 2025, +24% YoY, the first meaningful increase since the 2016 peak; linked to AI-assisted development tools. https://appfigures.com/resources/insights/20251205

[^7]: RevenueCat — State of Subscription Apps 2025. Nearly 30% of annual subscriptions are canceled in the first month; low-priced annual plans retain up to 36.0% of users after a year, versus 6.7% for high-priced monthly plans. https://www.revenuecat.com/state-of-subscription-apps-2025/

[^8]: Company closures and restructurings: Care/of — Yahoo Finance / TechCrunch, Care/of is shutting down (Jun 2024) https://finance.yahoo.com/news/care-shutting-down-120200829.html; Forward — Fierce Healthcare, Primary care player Forward shutters after raising $400M (Nov 2024) https://www.fiercehealthcare.com/health-tech/primary-care-player-forward-shutters-after-raising-400m-rolling-out-carepods; Modern Age — Longevity.Technology, Longevity clinic Modern Age announces closure https://longevity.technology/news/longevity-clinic-modern-age-announces-closure/; WeightWatchers — WW International Form 8-K / press release on its pre-packaged Chapter 11 (May 2025) https://www.sec.gov/Archives/edgar/data/0000105319/000119312525114307/d934787dex992.htm

[^9]: Business of Apps — Cost per Install (CPI) Rates research. Reported CPI rose from roughly $0.50–$2.00 in 2019 to a projected $1.75–$4.50 in 2024, with the top of the range climbing about 125%. https://www.businessofapps.com/ads/cpi/research/cost-per-install/

[^10]: WW International full-year revenue from company results and SEC filings: $1.41B (2019), $1.38B (2020), $1.21B (2021), $1.04B (2022), $889.6M (2023), $785.9M (2024); pre-packaged Chapter 11 filed May 2025. FY2024 results: https://www.globenewswire.com/news-release/2025/2/27/3034270/0/en/WW-International-Inc-Announces-Fourth-Quarter-and-Full-Year-2024-Results.html · revenue history: https://stockanalysis.com/stocks/ww/revenue/